This is one of the most common questions I get, and yes in short you can... for specific reasons. Each one has rules, timeframes, and consequences you need to be aware of. KiwiSaver is designed to be a long-term investment that benefits from the power of compound interest, so in theory the later you withdraw, the more there will be.

When can you withdraw your KiwiSaver money for a first home?

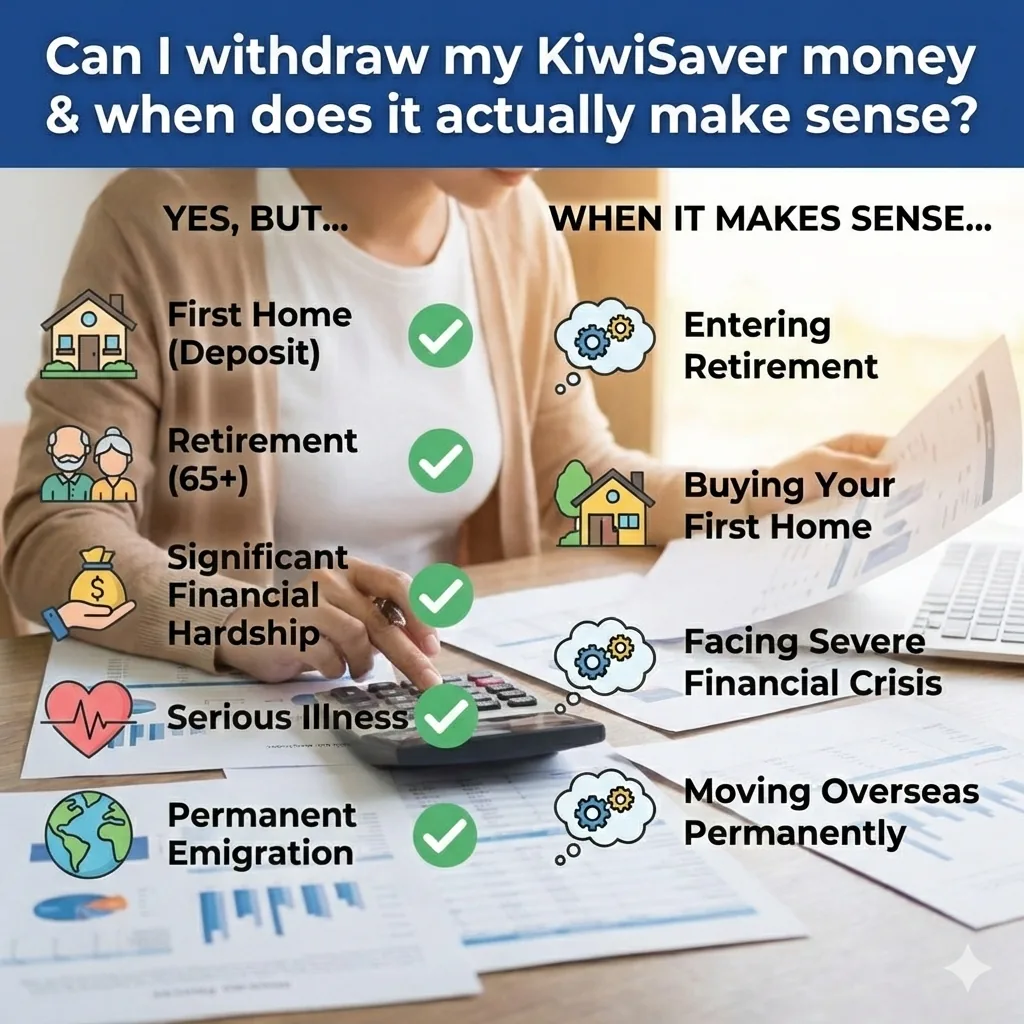

If you’re buying your first home, KiwiSaver can be what makes the deposit possible. You can usually withdraw everything in your account except for $1,000, after you have been enrolled and contribution into KiwiSaver for 36 months/ three years. They don’t have to be consecutive months.

The withdrawal process isn’t instant; there’s paperwork and legal steps your lawyer will go through with you, so the earlier you check your eligibility, the smoother things go when you actually find the right place. A quick review with me can help you avoid surprises and keep your purchase on track.

What If you’ve owned a home before - Can you still use KiwiSaver?

You can only use your KiwiSaver once for buying a house. If you have owned property before without using your KiwiSaver, and no longer own property there is a possibility of a ‘second chance.’ It depends on your current financial position and whether Kāinga Ora considers you to be in a similar situation to a first-home buyer. If you think you might qualify, it’s worth checking early - these assessments can take time, and leaving it until the last minute can cause unnecessary delays.

Can you withdraw your KiwiSaver money for hardship?

Yes, but it’s not something I ever want clients to rely on. Significant financial hardship withdrawals exist for situations where you genuinely have no other options.. its literally your last chance. Think essential living costs, overdue bills, or medical expenses. The criteria are strict, the evidence requirements are heavy, and approval isn’t guaranteed. If you’re considering a hardship withdrawal, it’s worth getting advice first, because it can seriously impact your long-term balance.

How do you check your KiwiSaver balance easily?

Checking your KiwiSaver balance is simple. You can log in to your provider’s online portal or app, and if you’re not sure who your provider is, you can find out through Inland Revenue using your MyIR account. It only takes a minute, and it’s the quickest way to see your balance, your fund type, and how your contributions are flowing in. Most Kiwis don’t check often enough - and staying in the wrong fund type for too long can cost far more than people realise.

If you don;t know who your provider is you can find out on the MyIR app or by calling the IRD. The IRD can show you who your provider is, but NOT which type of fund you are in. You can see how much money has been deposited into your KiwiSaver via your employer(s), but the total there will not be correct as they do not have live access to the investment earnings your fund has made.

What should you look for when you check your KiwiSaver account?

When you log in, you want to look at more than just the balance. Check your fund type, your contribution rate, and whether your returns match the level of risk you’re taking. Also take a quick look at fees and performance over several years - not just the last month. A few simple checks can give you a much clearer picture of whether your KiwiSaver is set up to support your goals.

Not sure If your KiwiSaver account is set up correctly?

If you’re unsure whether you’re in the right fund, contributing the right amount, or eligible to make a withdrawal, the easiest first step is to download my free eBook which goes into more depth about how KiwiSaver works. The next step after that is booking a meeting with me (which is also free) where i can answer any trickier questions that you have and make a plan tailored specifically for you.

Both can be found on my website:

Simple Steps. Solid Results

Written byCameron Steele, KiwiSaver Specialist & Financial Adviser based in Christchurch, New Zealand.

Get personalised KiwiSaver advice

Free 30-40 minute session with Cam. No obligation. Online anywhere in NZ or in person across Canterbury.

Book a free session