I want you to do a quick self-assessment. On a scale of 1 to 10, rate yourself on two things:

- How well do you understand KiwiSaver? (1 = no idea, 10 = completely across it)

- How likely are you to act on new KiwiSaver knowledge? (1 = unlikely, 10 = very likely)

If you want an objective starting point, the free KiwiSaver Knowledge Challenge gives you a score in a few minutes.

Got your scores? Here's what I find when I ask this question to the people I work with.

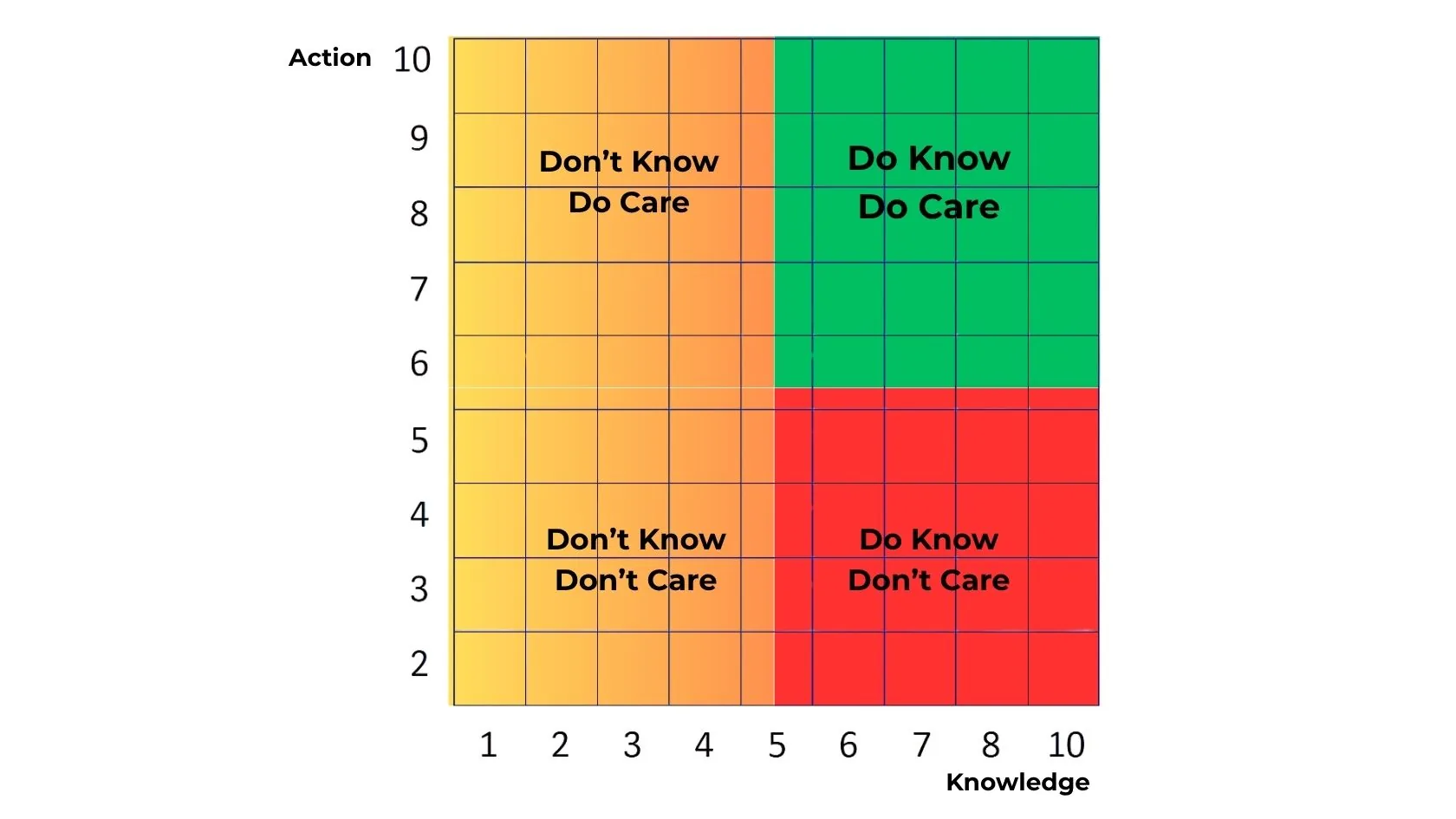

Where most people land

The majority of New Zealanders score somewhere between 2 and 4 on both scales. That's not a criticism - KiwiSaver is genuinely confusing, and most of us were never taught how it works. But it does mean there's a significant gap between where people are and where they could be.

If you map those two scales onto a grid, you get four quadrants:

- Bottom-left (low knowledge, low action): You're not sure what fund you're in or what it costs, and you haven't done anything about it. You're not alone - this is the most common starting point.

- Top-left (high action, low knowledge): You've made changes to your KiwiSaver, but without fully understanding what you were doing. This can lead to decisions like switching to a conservative fund during a market dip and locking in losses.

- Bottom-right (good knowledge, low action): You understand the theory but haven't pulled the trigger. Maybe you've been meaning to get around to it. This is actually the most frustrating quadrant to be in, because the gap between knowing and doing is costing you real money.

- Top-right (high knowledge, high action): You understand your KiwiSaver, you've made informed choices, and you review it regularly. This is the goal.

What a free session actually does

I run free 30 to 40-minute KiwiSaver advice sessions with New Zealanders every week. The goal of every session is to move people from wherever they are in that grid to the top-right quadrant.

In that time, I can help most people:

- Understand what fund they're in and whether it suits their situation

- See what their current contributions are actually building toward

- Identify whether they're missing out on government contributions

- Compare their provider against alternatives in the same risk category

- Decide on a clear next action - whether that's staying put or making a change

About 95% of the people who come through a session leave with both more knowledge and a concrete plan to act on. The confidence that comes from having clear, personalised information makes a real difference.

The 5% who don't act - and why

The remaining 5% leave the session with new knowledge but still don't act. The reasons I hear most often:

- "I want to wait until after the election."

- "I'm changing jobs soon, so I'll sort it then."

- "My balance isn't big enough yet to be worth worrying about."

- "I'll get to it when things settle down."

I understand all of these. But they're almost always reasons to delay, not genuine reasons to wait. Elections don't reset KiwiSaver rules overnight. Job changes are actually an ideal time to review - not a reason to put it off. And the smaller your balance, the more impact a good fund choice has as a percentage of future growth.

The best time to sort your KiwiSaver was years ago. The second-best time is now.

Where do you sit?

Go back to your two scores. If you're not already in the top-right quadrant, the gap between where you are and where you could be is real - and it's measurable in dollars.

A free session costs you nothing. There's no obligation to make any change. But for most people, it's the thing that finally moves them from "I should probably look at that" to "I'm glad I did."

Book your free session

30-40 minutes, no obligation, no cost. Online anywhere in NZ or in person across Canterbury.

Book a free sessionNo. Even with 15-20 years to retirement, optimising your fund and contributions now can make a significant difference. Compound growth still works in your favour, and there's often a lot of low-hanging fruit - wrong fund type, undercontributing, missing government credits, or being with a provider that consistently underperforms.