I usually keep these blogs simple & avoid finance jargon, but with everything happening globally at the moment - including the Iran war and rising energy prices - it’s worth looking a bit deeper at how events like this can affect KiwiSaver.

This is one of those situations where understanding how KiwiSaver funds actually work can explain why some members see more volatility than others, and why long-term strategy matters more than headlines.

In short, active managers of KiwiSaver, who look for opportunities at all times and can often do very well in geopolitical shocks.Passive managers that track the market closely will usually move with the market during shocks, while active managers may have more flexibility to adjust risk or positioning depending on their strategy.

For full disclosure, I work with five KiwiSaver providers that I believe offer strong long-term options. These providers use active management, which means they can adjust positions during market shocks rather than simply tracking an index.

The current Iran war has been felt in markets primarily through energy supply risk: the Strait of Hormuz is one of the world’s most critical oil and LNG shipping routes, and disruption there can push up global energy prices fast.

For KiwiSaver members, the day-to-day impact rarely comes from “New Zealand shares only”. It more often flows through six channels: your fund’s asset mix, the NZ dollar (FX), bond yields,commodity prices (especially oil), equity volatility, and investor fund flows.

In New Zealand, a sustained oil shock can also spill into inflation expectations and interest-rate pricing. The Reserve Bank of New Zealand has signalled it would be cautious about reacting to short-term oil spikes, but a prolonged shock that entrenches inflation could change the calculus.

Active KiwiSaver managers can add value in shocks (often via risk management rather than “war bets” on weapons companies etc)

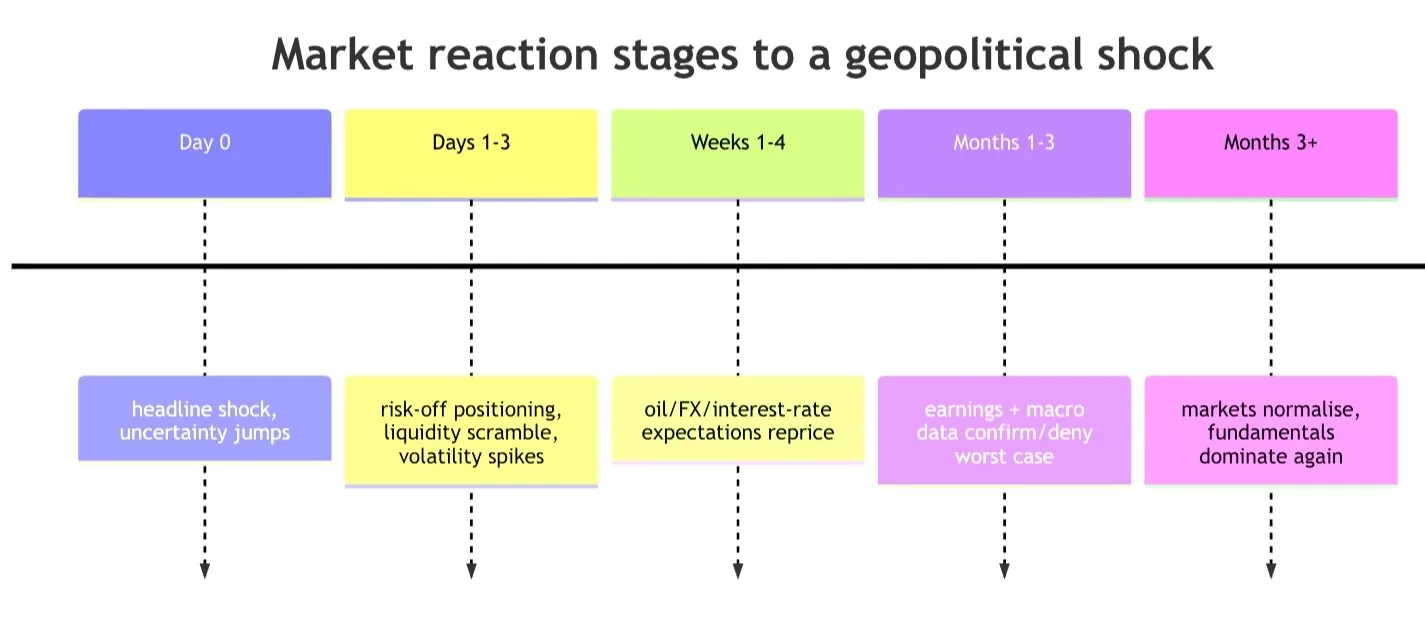

History also shows a consistent pattern: markets often price “worst case” first, then re-price as the path becomes clearer - sometimes quickly, sometimes not.KiwiSaver success typically comes from getting the long-term settings right (risk level, fees, diversification) and refusing to panic-sell your future.That’s why events like wars, inflation shocks, or market crashes usually matter less than people think - as long as your KiwiSaver fund is set up correctly for your timeframe and goals.

What’s happening and why markets care

News reporting on the war indicates it has materially disrupted regional energy logistics and triggered emergency policy responses, including strategic oil stock releases coordinated by the International Energy Agency.

Why markets fixate on Hormuz: the U.S. Energy Information Administration estimates that in 2024 oil flows through the Strait averaged ~20 million barrels/day - about 20% of global petroleum liquids consumption - and that roughly one-fifth of global LNG trade also transited the Strait (notably from Qatar).

That’s why energy prices can jump on risk of disruption (or actual disruption), even before broader economic data changes. The IEA has characterised the disruption as historically large and has emphasised that stock releases help, but restoring safe transit through Hormuz is pivotal.

A useful mental model is the “market reaction curve”:

If you only remember one line: KiwiSaver is a long-distance event, not a 100‑metre sprint with a live commentary track.

How a conflict like this hits KiwiSaver in practice

Asset allocation: your fund type does most of the heavy lifting

KiwiSaver funds are typically grouped by “growth assets” vs “income assets” (shares/property/alternatives vs cash/fixed interest).

Sorted’s fund-finder methodology groups funds roughly as: Defensive (0-9.9% growth assets), Conservative (10-34.9%), Balanced (35-62.9%), Growth (63-89.9%), Aggressive (90-100%).

In a geopolitical shock, that mix tends to explain why:

Growth/Aggressive funds usually bounce around more (more shares, more global exposure).

Conservative/Defensive funds can still fall (bonds can drop when yields rise), but often less.

The uncomfortable truth: if you want long-term growth, you can’t avoid short-term volatility - you can only choose how much of it you can live with.

NZD (FX): overseas returns get translated back into Kiwi dollars

Most diversified KiwiSaver funds hold a significant chunk of offshore assets, so your return is affected by:

what global markets do in their currency, and

what the NZD does when those returns are translated back.

The RBNZ explicitly treats the exchange rate as important in a small open economy, partly because it influences import prices and tradables inflation over time.

During “risk-off” episodes, research from the International Monetary Fund finds recurring patterns where the USD (along with JPY and CHF) tends to appreciate against other currencies. That matters because a falling NZD can cushion unhedged global share losses in NZD terms (but also makes imported costs - like fuel - more expensive).

Bond yields: inflation shocks can hurt “safe” assets too

Geopolitical energy shocks can raise inflation expectations. If markets think inflation will stay higher for longer, yields can rise -and bond prices generally fall.

That’s why diversified funds sometimes get hit on both sides: shares wobble and bonds fall (a classic unpleasant surprise). This dynamic was discussed in New Zealand market commentary during prior crisis periods and is central to how diversified portfolios behave when inflation risk dominates.

Commodity prices: oil is the loudest input

Oil is the main transmission mechanism markets are watching. The IEA’s large stock release was explicitly to address disruptions stemming from the Middle East conflict.

From a KiwiSaver perspective, oil matters because it can:

lift costs for airlines, freight, manufacturing, and households (lowering real spending power), and

change the inflation/interest‑rate outlook, which affects bonds and equity valuations.

Equity volatility: pricing uncertainty, not just “what happened”

A key point many investors miss: markets often move most when the story is least clear. In prior crises, analysts have documented large “down then up” swings as investors rapidly re-price potential scenarios.

Fund flows: where money moves can move prices

In shocks, investors often rotate from riskier assets toward perceived safe havens (cash, high-quality government bonds, reserve currencies). This “flight to quality” is widely described in finance education, and FX research shows repeated patterns during risk-off episodes.

These flows can create:

temporary dislocations (good assets sold for liquidity),

style rotation (e.g., “quality” vs “value”), and

sharper currency moves - all of which show up in diversified KiwiSaver balances.

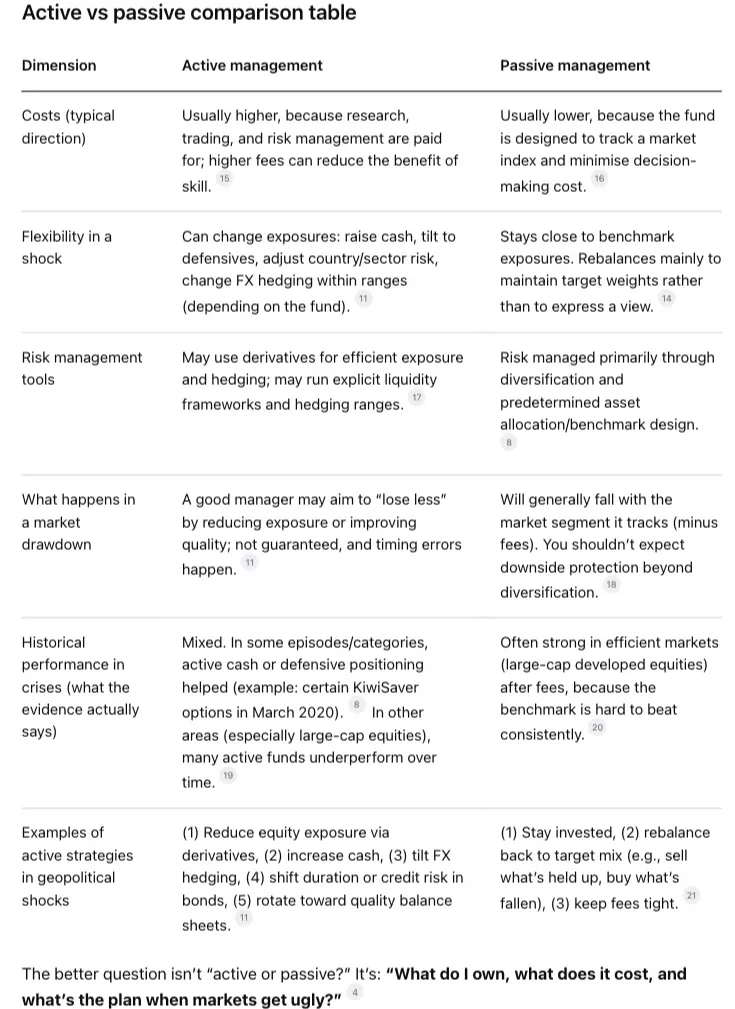

Active vs passive management when the headlines hit

The FMA’s plain-English distinction is a good starting point:active managers make decisions on what to buy/sell; passive funds track an index.

Here’s what that means in geopolitical shocks - where the goal is often risk management and avoiding permanent loss, not “making money from war”.

Active vs passive comparison table

Can active managers outperform in shocks without “profiting from war”?

Yes-sometimes, and the most credible examples usually look boring in hindsight: more cash, less leverage, tighter risk controls, disciplined rebalancing, and selective hedging.

But it’s not a free lunch. Independent scorecards show underperformance is common in many equity categories over time, and the odds worsen as fees rise.

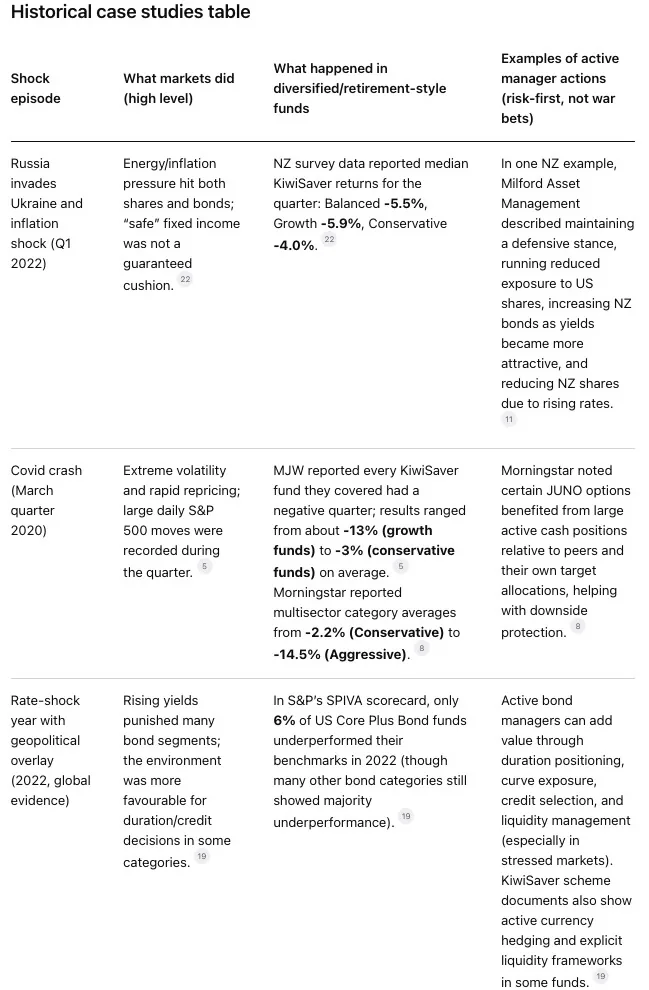

What follows are three evidence-based case studies (two NZ-centric) that show how outperformance can happen during volatile periods-without relying on war profiteering.

A key takeaway from the NZ case studies: outperformance often came fromcash holdings, hedging discipline, and avoiding forced selling- not from allocating to “war winners”.

That distinction matters ethically and practically. If a member wants to avoid certain industries (e.g., weapons), that choice is usually implemented through the fund’s responsible investment policy and exclusions - separate from the manager’s short-term risk controls.

Investor quotes that matter when markets are noisy

These are short on fluff and long on usefulness:

“Our goal is more modest: we simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

- Warren Buffett

“Price is what you pay; value is what you get.”

- Buffett (crediting Ben Graham).

“In the short run, the market is a voting machine; in the long run… it becomes a weighing machine.”

- Buffett (crediting Ben Graham).

“You can’t predict. You can prepare.”

- Howard Marks, Oaktree Capital Management

“The time of maximum pessimism is the best time to buy…”

- John Templeton (via Franklin Templeton’s “Templeton Maxims”).

If you read those slowly, you’ll notice the shared theme:process beats prediction.

Practical KiwiSaver actions to consider right now

This is general information (not personalised advice). The smartest move depends on your timeframe, goals, and how you sleep during volatility.

Re-check your timeframe before you touch anything

If you’re decades from retirement (or a first-home withdrawal that’s still years away), daily volatility is mostly noise; uncomfortable noise, sure, but noise.

If you’re within ~2-5 years of using the money, you should be extra wary of being in a fund that can drop 10-15% in a rough quarter (because you might be forced to “sell low” by needing cash). The 2020 quarter is a case study in how fast that can happen.

Don’t change risk level because the news is scary-change it because your life is different

A fund switch should usually be driven by:

you’re closer to spending the money than you thought, or

you overestimated your risk tolerance, or

your fund’s fees/strategy no longer make sense.

If you’re thinking “active vs passive”, make it a fee-and-proof conversation

If you pay active fees, you’re buying something: risk management, tactical tilts, security selection, FX decisions.

So ask for evidence in the places that matter:

How did the fund behave in drawdowns (e.g., 2020, 2022)?

What is the benchmark and how consistently is it used?

Are fees reasonable relative to the value delivered?

These are exactly the kinds of “value for money” questions the FMA has pushed the industry to answer more consistently.

In 2019 a large KiwiSaver provider was penalised for this practice - not a good look.

Look at currency hedging (because it quietly shapes your ride)

Some funds run explicit FX hedging ranges and may tactically adjust hedging levels; for example, one scheme document describes FX hedging monitored daily and implemented with derivatives, within defined ranges.

You don’t need to become an FX trader. You do need to know whether your global exposure is mostly hedged or not-because that changes how NZD moves affect your balance.

Rebalance thoughtfully (or let the fund do it)

If your fund is diversified, it’s already doing some version of rebalancing. The real risk is doing an emotional rebalance (selling growth after it fell, buying conservative after it rose).

Keep your information sources clean

In a crisis, your biggest investment risk is often your browser tab, not your portfolio.

Prioritise primary documents and official data; treat hot takes as entertainment.

Sources to prioritise and a ready-to-use content pack

Sources worth prioritising

Use these as your “high-trust stack” for any KiwiSaver + geopolitics analysis:

Official KiwiSaver fund updates / SIPOs / PDS (what the fund can do, what it actually holds, what it costs).

NZX announcements and corporate actions (company earnings, dividends, market disclosures) via NZX’s official channels.

RBNZ publications (OCR outlook, inflation drivers, exchange-rate channel).

Energy market primary sources (IEA releases, EIA chokepoint data).

Independent performance research and methodology notes (e.g., SPIVA-style scorecards; category-level active/passive evidence).

Reputable financial press for facts, then verify against primary sources.

Get personalised KiwiSaver advice

Free 30-40 minute session with Cam. No obligation. Online anywhere in NZ or in person across Canterbury.

Book a free session